The Parasitic Moral Hazard of Usury

Lending money at interest starts the slide down the slippery slope to unbridled exploitation, disintermediation, dispossession, and cultural collapse.

Following the unfolding debate about usury on Gottesdienst has been an education. Rev. Vincent Shemwell of Bethlehem Lutheran Church in Johnson City, TN, has made the case against usury1, while Pr. Travis Berg of Bethel Lutheran Church in Lander, WY, has declared for it2, with an assist from Rev. Dr. Ben Mayes from CTFSW3.

It’s not just an academic discussion for Lutherans, as the LCMS operates a money lending subsidiary, the Lutheran Church Extension Fund (LCEF), which has a $1.62 billion loan portfolio and $235 million in net assets. The ELCA equivalent is the Mission Investment Fund (MIF), which has a loan portfolio of $610.5 million and net assets of $212.8 million. The WELS Church Extension Fund has a loan portfolio of $203.4 million and net assets of $130.3 million.

Guided evolution

The Lutheran position on usury has evolved significantly, shifting from Martin Luther’s harsh condemnation of all interest-bearing loans4 to Johann Gerhard's distinction between fair and exploitative lending, and ultimately to today’s laissez-faire approach, which is fully coupled to and dependent on supranational money and credit structures. Luther, ever the Christian Nationalist, was so violently opposed to usury that he asked for civil as well as church sanctions, including the major ban, and a denial of baptism or burial for usurers unless they repented (hard to do when you’re dead…).

“I cannot rest, I cannot stay, I cannot linger anywhere. My spirit never walked beyond our counting-house—mark me!—in life my spirit never roved beyond the narrow limits of our money-changing hole; and weary journeys lie before me!”

A Christmas Carol, by Charles Dickens

Usury was understood as any financial interest charge above the principal value of a loan. Today’s definitions have become increasingly murky; the only negative connotations are associated with “predatory” financial practices. However, it is notable that, historically, all usury was considered predatory, and it was illegal across many cultures and religions, including Hinduism, Buddhism, Judaism, and Islam, as if written into the hearts of all men from creation (Romans 2:15).5

For Christians, usury was frowned upon because it was considered unearned income, “a cousin to theft”. The church valued tangible work and production (by the sweat of one’s brow) as essential to initiative, enterprise, efficiency, and an ordered, Godly society. Usury was the opposite: wealth acquired with no labor, minimal expense, and little risk on the part of the lender, who didn’t even have to be in the same town as the borrower. For Thomas Aquinas, the moneylender was selling the same thing twice, echoing Aristotle’s statement that "a piece of money cannot beget another".

It was only in 1917 that the Roman Catholic Church modified its prohibition on usury6. Lutherans had a much earlier head start with Johann Gerhard and Martin Chemnitz justifying and excusing lending at interest. However, Gerhard only tolerated lending for profit if the end-user intended to deploy the capital in a for-profit venture (productive vs unproductive loans). He certainly would have taken a whip to the compounding and amortization tables beloved of the finance bros. For the destitute, he expected gifts to be made. For the indigent, he expected zero-interest loans on flexible terms. Who will not notice that modern lenders do not offer meaningful capital gifts to the poor or no-interest loans on flexible terms to the indigent?

The shift in Lutheran orthodoxy regarding usury is complete. We, along with most of the world (Islamic countries have made some half-hearted attempts to retain at least a nominal ban on usury), have moved from rejecting and outlawing usury to tolerating interest-bearing loans in limited circumstances, to shrugging at high-interest, compound loans on even essential consumption items. Church lending and banking have become so thoroughly enmeshed in the global financial system that their business practices are indistinguishable from the hustle of the Money Trust. The distinction between loansharking and pinstripe banking is now merely a matter of a regulator’s stamp of approval.

“Shall I not have barely my principal?”

Shylock, Merchant of Venice.

Primed for prime rates

Even the secular world recognizes that people are uniquely vulnerable to financial exploitation. Consequently, governments around the globe used to be careful to shield their citizens from the insatiable appetites of bankers. However, here in the United States, there was a relentless effort to chip away at the nation’s founding moral and regulatory restraints on usury7. We are now at the point where predatory lending bear traps have been set in every corner of the economy, so that the poorest households pay net interest, while the richest receive substantial net interest.

Worldwide, money lending has been the pernicious agent for unwanted social, cultural, and economic upheaval, deliberately harnessed to the ineluctable disaster that is the cult of Liberal Democracy8. For example, inflation rather than currency stability is the deliberate monetary and economic policy. That is then used to justify charging interest to maintain the purchasing power of the original principal. The very people who are responsible for debasing the currency have the gall to demand that you pay for their engineering that erodes your earnings. To ensure the punishment is fully felt, they steal more through “hedonic adjustments” and other shady tactics closely tied to tax and entitlement schemes, as evidenced by the steady increase in all taxes and promises to provide more free things to more people, which can only be debt-financed. Similarly, our ability to be constantly at war is primarily a byproduct of debt finance schemes that intentionally shift risk onto our children’s children.

A critical aspect of Liberal Democratic coercion has been the centralization of monetary and credit policy, deliberately abstracting it from familial, cultural, domestic, and national concerns. Until very recently, the City of London used LIBOR9 to manipulate borrowing costs worldwide for its own benefit, influencing everything from consumer loans to complex derivatives. It was only due to the discovery of criminal rigging of LIBOR (paralleling the manipulation of the London Gold Fix) that space was created for the United States to regain some control over its own money through SOFR.

This conforming coercive power of Liberal Democracy is how Americans at large and the church specifically capitulated and fell in line with consumerist fixation that necessitated relentless debt accumulation. On the “conservative” side, the soothing assurances of William F. Buckley, Milton Friedman, Ayn Rand, and Murray Rothbard have been, in terms of outcome, identical to the prescriptions of Noam Chomsky, Joseph Stiglitz, Simone de Beauvoir, and David Graeber, respectively. We all arrived at the same miserable destination, despite the supposed polarity of the politics, and that is because politics is downstream from power, not culture.

“With money, Varenka, one can buy respect, even kindness; without it, you are nothing but a worm underfoot." Fyodor Dostoevsky, Poor Folk (1846)

" Credit is a trap; it’s the promise of money that doesn’t exist yet, and it binds you tighter than any chain." Fyodor Dostoevsky, The Gambler (1866)

Money is coined liberty, and so it is ten times dearer to a man who is deprived of freedom." Fyodor Dostoevsky, Crime and Punishment (1866)

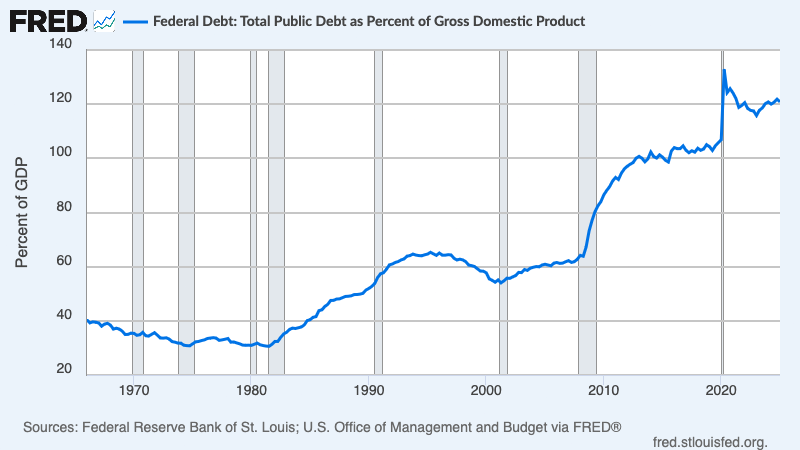

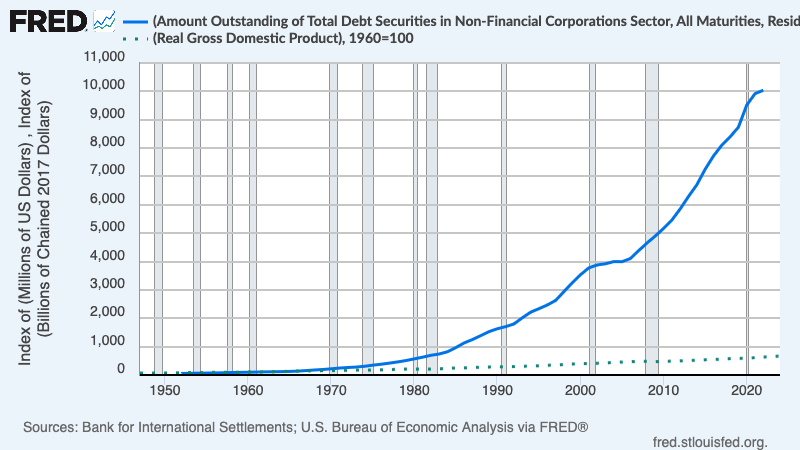

The most visible evidence of the malign effects of easing usury constraints has been the surge in private, corporate, and government debt. Much of our declared debt is obscured by Enron-inspired accounting tricks, keeping gargantuan unfunded liabilities hidden by not reporting them (we are on the hook for nearly $165 trillion, ~$1 million per taxpayer). As a nation, we have been reduced to Esau, prioritizing the utility and prosperity of the present generation over that of future generations. It is the most odious intergenerational larceny, as our descendants' inheritance is mortgaged a thousand times for a facile illusion of wealth this instant. It is the inevitable outcome of maniacally discounting future values, inherent in the compounding interest function.

Unfortunately, the church has gone along with elegant docility and subservience, perfectly described by Ryszard Legutko in The Demon in Democracy: Totalitarian Temptations in Free Societies:

“The aim of the conciliatory Christians has been to avoid conflicts with the liberal democrats and to adapt themselves to the existing system, which they thought sufficiently spacious and friendly to include Christianity together with other religions. The aim of the Christians who have capitulated is to be admitted to the liberal democratic club, and in order to do it, they are willing to accept any terms and concessions, convinced that remaining outside the club or being refused entrance would bring infamy on them.”

Retvrn to the Fathers

Lending at interest will not be overturned soon, if at all, because the entire global financial system is a perfidious rhizome nourished by compound interest and cultivated by masters of the universe you don’t know and would never trust in your own home. However, we can acknowledge a profound and detrimental shift in the understanding and acceptance of usury, particularly since Christianity has been co-opted and conformed to be of the world in the spheres of money, finance, and politics.

Where usury was once condemned as an unequivocally harmful, exploitative, and immoral practice, it has been almost entirely reversed in modern times. The results have been profoundly negative for society and are a root cause of the church’s decline and loss of moral authority. Similarly, the debt machine has been very effective at stripping national sovereignty and agency, placing the welfare of billions of people in the hands of bond market buccaneers who have zero interest (excuse the pun) in Christian charity.

We should at least be honest about the fundamental moral contagion of usury, even as we indulge in casuistry about its pragmatic benefits and inescapable realities. The truth is that lending at interest is a key driver of systemic economic exploitation, unsustainable debt, and the profound compromise of religious institutions that once stood in opposition to it.

As Christians, we should be concerned about developing Kosher loans and capitalization practices that match the text, intent, and spirit of Scripture. Grace is free, money is not, but perhaps the church can be more like Matthew the Disciple rather than the Tax Collector.

Luther was incensed by speculators profiting off the poor during the inflation and famine in Wittenberg in 1539. He equated usurers with "mass murderers" for depriving people of necessary sustenance. Luther did approve of the "purchase of rental income" (inskauf). This workaround enabled a perpetual payment in return for a lump sum, similar to a rental contract on property, which was viewed as distinct from a direct, interest-bearing loan on money itself. However, even this approved product was often misused and approximated standard interest loans.

Dante’s Divine Comedy reserves the inner ring of the seventh circle of Hell (violence against God) for blasphemers, sodomites, and usurers. On a barren and sandy plain, groups of spirits adopt different postures, suffering showers of flakes of fire that fall on their naked bodies and set the sand on fire underneath them. Blasphemers lie flat on their backs, sodomites are in constant motion, and usurers crouch with purses strung from their necks.

Usury Laws by State, Interest Rate Caps, The Bible & More. https://wallethub.com/edu/cc/usury-laws/25568

1864: National Bank Act

The Supreme Court's interpretation of this act later preempted state usury laws, creating a path towards a national consumer lending economy

1970s: Effective Deregulation Begins

Deregulation of usury laws, particularly affecting credit cards, started around this decade.

1978: Marquette National Bank v. First of Omaha Service Corporation Supreme Court Ruling

This was the most significant federal case in the deregulation of credit card interest rates. The Supreme Court ruled that nationally chartered banks could charge the legal interest rates of their home states and "export" those rates to customers in other states, even if those states had lower usury limits. This interpretation of the National Bank Act meant that state usury laws did not apply to nationally chartered banks.

1980: South Dakota Eliminates Usury Laws

South Dakota became the first state to completely eliminate its usury laws, attracting Citibank to relocate its credit card division there in 1981

1980: Depository Institutions Deregulation and Monetary Control Act (DIDMCA)

This act granted state-chartered banks the same right as nationally chartered banks to "export" their interest rates. This meant that all FDIC-insured banks could charge the highest permissible interest rate in their home state to out-of-state customers, regardless of the customer's location. States responded by passing "wild-card" or "parity" statutes to grant state banks similar privileges

1982: Most States with Biggest Banks Eliminate Usury Ceilings

Following South Dakota's lead, states like Delaware repealed their usury laws, leading to a competitive response where most states with major banks had abolished their usury ceilings by 1982. This led to credit card companies serving a previously ignored market of low-income, high-risk borrowers

1996: Smiley v. Citibank Supreme Court Case

The Supreme Court upheld Citibank's justification that a late fee on a credit card bill was considered "interest" under the National Bank Act, making such fees immune to state regulation. This ruling led to an increase in late fees and other charges

1999: Gramm-Leach-Bliley Financial Modernization Act

Section 731 of this act specifically targeted Arkansas, allowing local banks to assess the same rates charged by national banks with locations in Arkansas, effectively overriding the state's constitution regarding usury limits

2009: Credit CARD Act

This act, passed by the Federal Reserve Board, capped late fees at $25 per transaction, providing some re-regulation in this specific area.

Ryszard Legutko’s The Demon in Democracy: Totalitarian Temptations in Free Societies is an incredible examination of Liberal Democracy, which parallels Communism with its utopian grand design ideology that suppresses dissent and ultimately elevates mediocrity. Like Communism, Liberal Democracy politicized every aspect of life, including culture, family, and even religion, as both systems seek total control over thought and action. In both ideologies, we find that freedom and independent thought are sacrificed for systemic control and manufactured consensus.

Christians have increasingly been suppressed by legislated morality (abortion, gay marriage, legalized drug use, lifting usury restrictions, euthanasia, etc.) in open confrontation with Scripture and the Church. The intended result is the steady marginalization and secularization of Christianity in the public sphere, confining it largely to inner and family life and demanding that all religions demonstrate their support for the liberal order (the "post-war consensus").

Modern philosophers, such as Hobbes and Locke, sought to reinterpret Christianity in a manner that was palatable to contemporary men, free from "scholastic philosophy," and aligned with the new scientific achievements of their time. This effort is described as a paradox, "intermingling coercion with liberation," by forcing religion to conform to a new political rationality. Rousseau's concept of "civil religion" further solidified this by proposing an artificial religious construction solely to serve a political purpose, superseding traditional forms of Christianity.

LIBOR (London Interbank Offered Rate) represented the average interest rate at which major global banks lent to one another in the interbank market. It was calculated daily across multiple currencies (e.g., USD, GBP, EUR) and maturities (overnight, 1 month, 3 months). As the global reference rate, LIBOR was the foundation for pricing financial products, including loans, mortgages, bonds, derivatives, and other credit instruments. ‘A guide to LIBOR - Its history, impact, and future’ https://www.corlytics.com/regulatory-hub/a-guide-to-libor-its-history-impact-and-future/

SOFR (Secured Overnight Financing Rate) was introduced by the Federal Reserve Bank of New York as a benchmark rate based on actual transactions in the U.S. Treasury repurchase (repo) market, where banks and investors borrow or lend using Treasury securities as collateral. Unlike LIBOR, SOFR is a secured rate (backed by collateral) and reflects overnight borrowing costs, making it less volatile, more robust, and representative of American market conditions. It is the dominant pricing mechanism for all USD securities. ‘Secured Overnight Financing Rate (SOFR) Definition and History’ https://www.investopedia.com/secured-overnight-financing-rate-sofr-4683954

I’ve been thinking on usury for quite a while, can’t avoid what the Bible says about usury, there is a prohibition.

The other unfortunate topic that kind of goes hand in hand with usury is indentured servitude/slavery for no more than a 7 year term, to pay off debts. There were instances the slave remained serving in the household after being granted freedom, because of the righteous and benevolent master, who was fair. This is not to say that this institution wasn’t grossly abused as it was. (See the story of Laban and Jacob). Not trying to advocate for slavery, but like usury, a topic that has been ignored

In Latvian there is a saying "Debt is not a brother." It, at the very least, should not be treated as one.