Rent or a Tithe? Don't Mess with the IRS

Unrelated Business Taxable Income (UBTI) is one of the most dangerous pitfalls for churches.

There is a simple question that every LCMS congregation sharing its facilities with another organization should be able to answer: Is the money we receive from it rent or a donation?

The distinction is not academic; it is the line between tax compliance and a potentially serious tax liability.

At an LCMS congregation in Maryland, a guest organization (an independent, non-denominational Pentecostal church with a different confession of faith) makes regular, predictable financial payments to the host congregation. These payments appear to be substantial as a proportion of overall income.

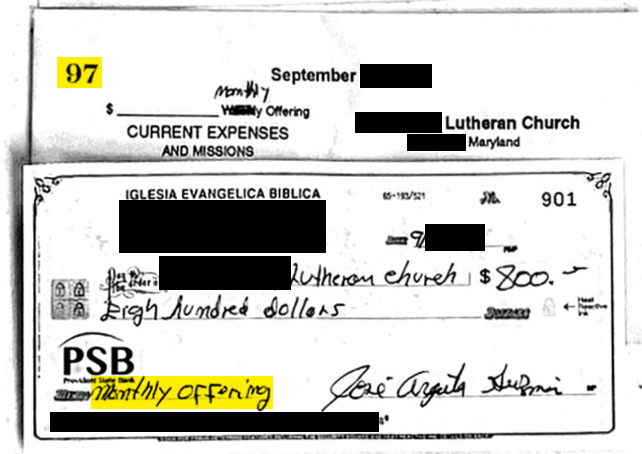

What makes this arrangement alarming is that guest congregation payments arrive in numbered giving envelopes. There is no exchange of invoices; only numbered giving envelopes, identical to those issued exclusively to individual members of the LCMS congregation for tracking their charitable donations. The guest church receives its own numbered envelope box (No. 97 in this particular year) each year, placed alongside the individual congregants’ boxes in the narthex for direct pickup. Members, including the guest congregation, receive separate annual statements of account recording their annual giving via the envelopes.

The question to be resolved is the purpose of the payment mechanism.

Classification Matters

Under the Internal Revenue Code, the distinction between a donation and a business payment is a substantive matter that churches game at their peril. For example, a congregation in the Denver area failed to pay taxes on income received from renting out its facilities to a third party. When the IRS found out, the building had to be sold to pay the outstanding taxes, penalties, and fines. The congregation no longer exists and was unable to hold a final service to deconsecrate its building because control had effectively shifted to its insurer, which barred access before the service.

A donation or gift, under common law and IRS precedent, is a voluntary, spontaneous transfer made out of “detached and disinterested generosity” (Commissioner v. Duberstein, 363 U.S. 278, 1960). It is not made in exchange for goods, services, or access, and it must not carry an expectation of a quid pro quo.

A rent payment is a regular, predictable remittance made in exchange for the use of property. When the payor receives designated space, scheduled access, storage, equipment use, and other facilities in return, the payment is rent, regardless of what the parties choose to call it.

The guest congregation at this LCMS church receives use of the sanctuary, narthex, audio-visual equipment, musical instruments, storage areas, an office (which is locked and inaccessible to the host congregation’s own members), kitchen facilities, classrooms, and whiteboards. These accommodations are documented in a Memorandum of Understanding (MOU). The MOU itself describes the financial arrangement using the words “donations and tithes”. The language that would be unremarkable if the payments were genuinely charitable, but it may become evidence of deliberate misclassification when the payments appear to be a form of compensation for the use of property by the measures typically applied by the IRS.

A financial fraud investigation expert described the situation as, “It is basically compensation, disguised as charity.”

A Constitutional Impossibility

There is an additional problem that makes the “donation” characterization not merely implausible but constitutionally impossible.

The LCMS congregation’s own governing documents restrict membership to natural persons. Corporate entities, including other churches, non-profits, Boy Scouts, sports leagues, etc., are not eligible to be members of the congregation. Only individual members are issued numbered giving envelopes, because only individual members as natural persons can make tax-deductible charitable contributions that the congregation tracks and acknowledges for tax purposes.

The guest church, as previously noted, is a separately incorporated religious organization that the LCMS congregation also treats as a “mission” it sponsors (yet which gives money to the LCMS congregation…). It is not a member, and it cannot be a member by any definition or creative construction. And, yet, it has been issued the very instrument, a numbered giving envelope, that declares to the IRS and real members that it is a bona fide member. The arrangement treats a corporate entity as if it were a congregant dropping an offering in the plate, when in fact it is a tenant paying rent for the use of a facility.

This is not a gray area. A corporate entity that cannot constitutionally be a member cannot constitutionally make a “donation” that is tracked and processed through the same system used for members’ charitable gifts. The congregation has forced a square peg into a round hole, and the reason seems obvious: calling it a “donation” is mutually beneficial.

Who Benefits from a Misclassification?

It is difficult to place the best construction on the arrangement as an innocent or convenient bookkeeping choice. In our opinion, it resembles a cooperative arrangement that may result in potentially improper tax benefits for both organizations.

For the guest church, classifying its rent payments as “donations” to a 501(c)(3) entity may allow it to present those payments to its own congregants as charitable giving rather than as an overhead cost. The question of how the guest congregation classifies these transactions on its own books remains unanswered.

For the host LCMS congregation, classifying the payments as “donations” allows it to avoid reporting the income as Unrelated Business Taxable Income (UBTI) under IRC § 512. Churches are generally exempt from federal income tax under IRC § 501(c)(3), but they are not exempt from tax on unrelated business income. Rental income from the regular use of church property by an outside organization is a textbook UBTI trigger, particularly when the arrangement involves designated space, scheduled access, and ongoing services.

Further, as whistleblower X pointed out to congregational leadership, a church may be required to pay income tax on the rental of personal property (chairs, tables, any type of mobile equipment) when the income exceeds $1,000 during any given year. X specifically cited the requisite IRS Form 990-T being used to report that income.

An additional warning X repeatedly emphasized was the issue of Private Inurement. X warned that if a group or individual renting the building is considered a disqualified person by the IRS, the church could face an excise tax of up to 225% of the benefit's value. A disqualified person is “any individual who was in a position to exercise substantial influence over the affairs of the applicable tax-exempt organization. Family members of the disqualified person and entities controlled by the disqualified person are also disqualified person.”

Therefore, X warned that a disqualified person could include someone with a financial interest who is renting the facility. The guest congregation has significant influence over the LCMS congregation: they are free to come and go at any time, and are often present during host congregation activities, as personal witnesses have observed. Most of the guest congregation’s requests are approved by the LCMS leaders, as shown in the minutes of the Trustee Meetings. The host church members are told that because the guest congregants “clean the building,” the “sharing” arrangement is perfectly acceptable.

Unrelated Business Taxable Income

The host congregation’s Board of Trustees has reportedly asserted that rental income constitutes UBTI only when the underlying property is debt-financed. This is a misstatement of the law. While IRC § 514 does address debt-financed property specifically, the threshold question under § 512 is whether:

the income derives from a “trade or business”, and

that is “regularly carried on”, and

is “not substantially related” to the organization’s exempt purpose.

Regular rental of church facilities to a non-LCMS organization with a different confession easily meets all three tests.

IRS UBTI enforcement is neither rare nor gentle. When a tax-exempt organization fails to report unrelated business income, the resulting liability includes not only the unpaid tax but interest, penalties, and in egregious cases, potential revocation of tax-exempt status. For a congregation already operating with a significant funding gap and minimal reserves, an IRS assessment is likely to be existential.

A critical distinction that church leaders often misunderstand, and that the leadership at this congregation appears to misunderstand, is the difference between Form 990 and Form 990-T. LCMS congregations, as churches, are automatically exempt from filing the annual Form 990 informational return that other 501(c)(3) organizations must submit. This exemption is frequently, and incorrectly, taken to mean that churches have no federal filing obligations whatsoever. That is incorrect. When a church receives unrelated business taxable income (unrelated because the income is not generated in the ordinary course of the congregation’s established activities per its Constitution and Bylaws), it must file Form 990-T and pay the tax owed, regardless of its Form 990 exemption status. The two obligations are entirely independent.

The whistleblower made this exact point to the incoming pastor in 2023, explaining that while the congregation was exempt from Form 990, it remained obligated to report and pay taxes on any unrelated business income. The warning was ignored. If the congregation has been receiving what amounts to rental income for years without filing Form 990-T, each unfiled year constitutes a separate compliance failure, carrying its own penalties and interest.

A Suppressed Review?

In February 2025, a qualified CPA was engaged to conduct a financial review of the congregation’s books. There is no apparent evidence that an engagement letter was signed, and the review was never completed. Credible accounts indicate the CPA’s work was not completed under circumstances suggesting it may have been obstructed by congregational leadership.

It is difficult to avoid the inference that the suppression of the CPA review is connected to the UBTI exposure. In our opinion, a professional financial review would immediately identify the misclassification of rental income as charitable donations. It would likely identify the numbered-envelope system as the mechanism behind that misclassification. And it would probably identify the congregation’s failure to file Form 990-T (the return for unrelated business income) as a compliance failure with potentially severe consequences: the congregation owns a property appraised at approximately $2.3 million, with no remaining mortgage. That is the asset the IRS would look to if the tax bill comes due.

Looking Ahead

The path forward is not complicated, but it requires honesty that has been absent thus far.

The congregation should obtain a thoroughly independent professional determination of whether the payments from the guest church constitute rent or donations under applicable IRS standards. Given the regularity of the payments, the quid pro quo of facility access, the MOU’s own terms (not least the guest congregation using the church address as its legal domicile on all regulatory filings), and the constitutional impossibility of a corporate entity making a “donation” through the membership envelope system, the answer seems clear.

If the payments are rent, the congregation must file amended Form 990-T returns for all open tax years, report the income, and pay the tax owed. It should engage qualified tax counsel immediately to negotiate a voluntary disclosure with the IRS before the agency discovers the problem on its own, which is highly probable given a recent immigration incident involving the guest congregation. Voluntary disclosure is treated far more favorably than discovery during an audit, as X has repeatedly underscored to leadership over the past several years.

Given the District President's constitutional supervisory authority over the congregation, these questions should have been asked and answered long ago. “The orderly and faithful processes the Church has established” do not include a process for ignoring federal tax law. That said, the pastor and officers of the congregation are the first point of responsibility.

Desperation all the way around. The membership's giving of leftovers instead of first fruits requires a Lutheran congregation to seek income from renting to stay afloat. Renting to advance a false teaching church to boot. We are reaping the whirlwind. It is not uncommon and it is just delaying demise, for the Lord will not be mocked.

Romans 13:7

[7] Pay to all what is owed to them: taxes to whom taxes are owed, revenue to whom revenue is owed, respect to whom respect is owed, honor to whom honor is owed.